A perfect score: 29 out of 29 cohorts survived.

Drop the withdrawal rate from 5% to 4% and the Gilded Age goes from remarkable to flawless. This animation shows every retirement cohort from 1871 to 1899 racing head-to-head — $1,000,000 starting balance, $40,000/year adjusted for inflation, 60/40 portfolio — and not a single one runs out.

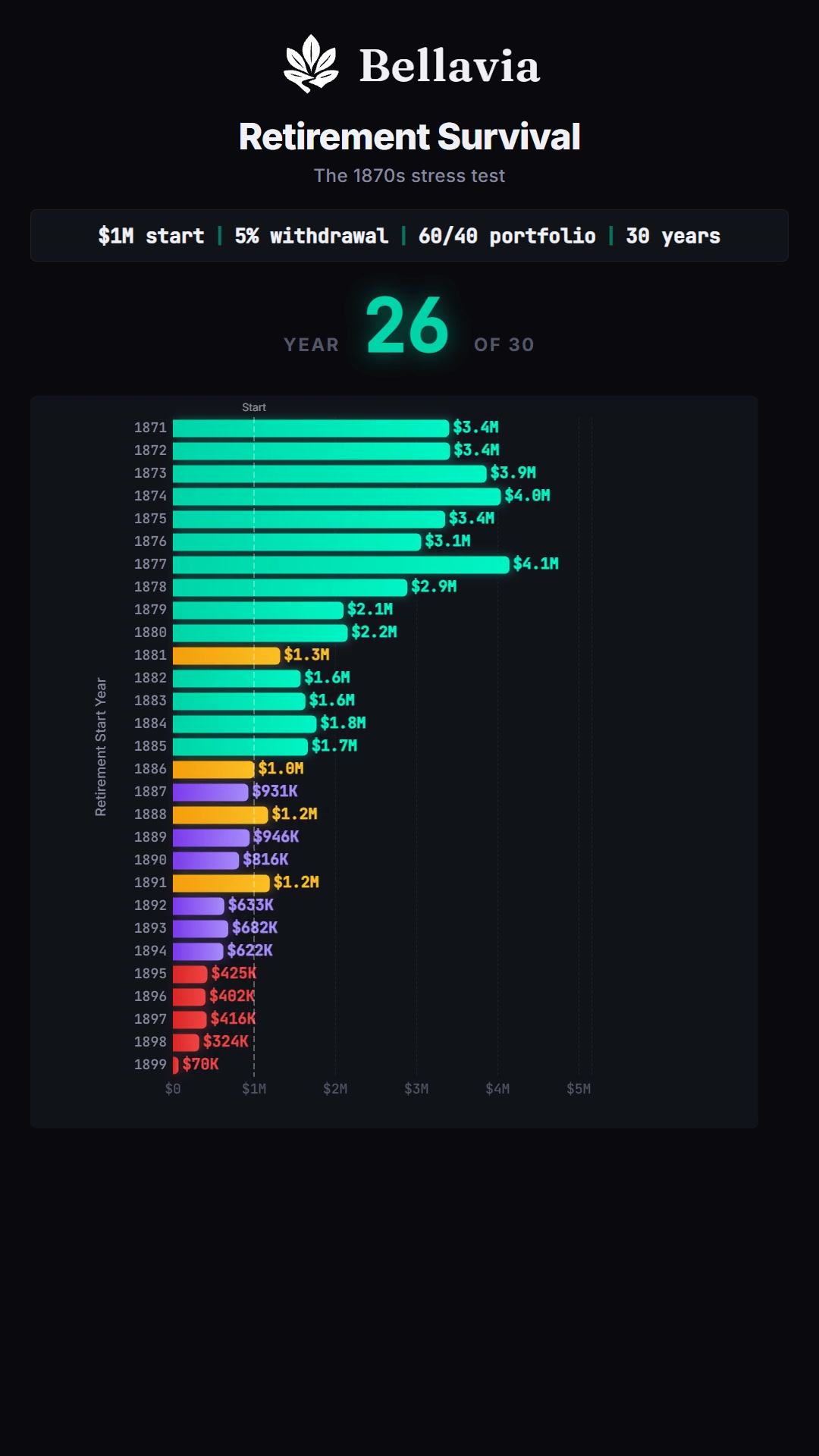

What stands out

At 5%, this era posted 97% survival. At 4%, there's no contest. The extra $10,000 left invested each year compounds through decades of deflation-fuelled real returns.

Most cohorts didn't just survive — they finished richer than they started. The combination of falling consumer prices, strong bond yields, and sustained equity growth made 4% withdrawals essentially risk-free in this era.

The critical question the video raises: the 4% rule was built for conditions like these. Will the next 30 years look anything like 1871–1899?

Try this scenario in Bellavia's retirement calculator.