(A version of this article was originally published as a guest contribution on Kitces.com — Nerd's Eye View.)

In retirement planning, a retiree's target retirement date often functions as the starting point for the rest of the analysis. Once that date is on the table, the conversation usually turns to the familiar levers planners can adjust, such as spending, allocation, and flexibility. Much of the retirement income literature focuses on adjusting those same levers once the planning process begins. But before any of these decisions come into play, there's another variable that may have an outsized effect on retirement outcomes: the date the retiree actually stops working. Even a modest amount of flexibility around that date may materially change the market environment a retiree enters, and with it, the sustainability of the plan.

Consider two retirees with identical portfolios. Both start with $1M in a 60/40 portfolio. Both plan to withdraw 4% per year, adjusted for inflation. Their plans are identical in every way except one: Retiree A retires at the end of 1973, and Retiree B retires at the end of 1975. The paths that follow turn out to be completely different.

Retiree A begins withdrawing during the 1973–74 oil crisis. What follows is double-digit inflation and low real returns. Retiree B, retiring only two years later, begins withdrawing after the worst has passed and rides a recovery that accelerates into the great bull market of the 1980s. After 30 years, Retiree A finishes with $278,000. Retiree B finishes with $3.36 million. These retirement paths are separated by just two years.

Far from this being the exception, the data show similar things happening across different historical cohorts. This raises some interesting questions: How much does the retirement date matter? Why does the literature spend almost all its effort on withdrawal rates and asset allocation? Are there alternative approaches available?

Using a variance decomposition across 97 historical 30-year cohorts from the Shiller dataset, the analysis estimates how much retirement timing matters relative to the strategies planners commonly suggest. For otherwise identical retirees starting with equal portfolios, allowing for a two-year flexibility window around the retirement date improved median portfolio outcomes by roughly 40%. When accumulation and withdrawal periods are linked into complete historical lifecycles, the same flexibility produces a substantial gap between the best and worst timing choices, with a median gap of roughly two-thirds in final portfolio value, with delaying retirement often leading to better outcomes. In some cases, these timing effects are larger than the improvements produced by more familiar levers, including changes to withdrawal strategy, equity allocation, or applying guardrails.

Why Retirement Timing May Deserve A Larger Role In Retirement Risk Analysis

Research on safe withdrawal rates – introduced by Bill Bengen and later extended by Wade Pfau, Michael Kitces, David Blanchett, and many others – has given planners a widely used framework for setting initial spending levels. The literature has also explored different dynamic strategies – guardrails, constant-percentage rules, variable-percentage withdrawals – to address the risk that a spending plan proves inadequate in an uncertain world. At the same time, researchers have examined how different equity-bond allocations across the retirement period affect portfolio sustainability.

Underlying this work is an assumption that is rarely examined. When a retiree says, "I want to retire in year Y", the planning task starts from that fixed point. This influences the withdrawal rate, the selection of allocation, and the choice of dynamic rules. The date itself is often treated as a life decision, rather than a financial one.

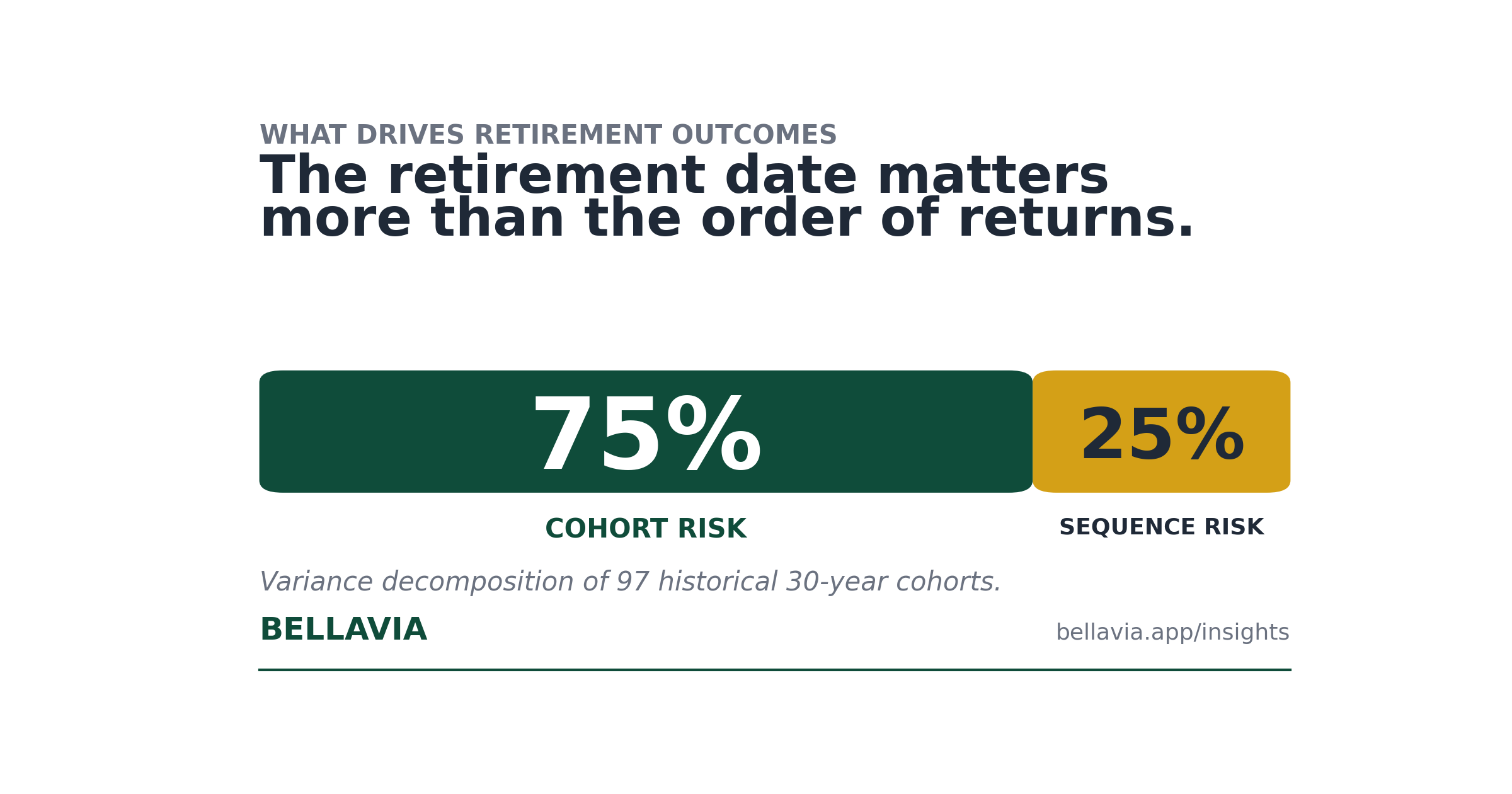

A variance decomposition of historical retirement outcomes suggests that this assumption may be worth reexamination. When the retirement date is included as a variable rather than a constraint, it turns out to be the single highest-impact lever we have tested in this historical analysis by a considerable margin.

How A Two-Year Shift Can Move Retirees Into A Different Return Environment

To test the value of retirement-date flexibility, our analysis connected 30 years of accumulation with 30 years of decumulation for every possible lifecycle in our dataset. During the accumulation phase, the model assumes annual real contributions of $10,000 invested in the S&P 500. During retirement, the retiree withdraws 4% annually, and follows a 60/40 allocation.

For each lifecycle, five retirement dates were simulated: the default (retire after exactly 30 years of saving) and four alternatives (one or two years earlier or later), each followed by 30 years of withdrawals. The two-year range in either direction requires up to 62 years of contiguous data, yielding 65 complete lifecycles for comparison (there are 67 possible).

As shown below, retiring one to two years early was the optimal outcome in only 21% of the historical lifecycles examined, compared with 64% in which delaying retirement by one to two years produced the best result. This suggests that flexible retirement is worth more than a year or two of contributions. Timing matters because withdrawal strategies, guardrails, and allocation changes all operate within a given market cohort, which means they primarily address variation in the ordering of returns. The variability is much larger between cohorts than within the cohorts themselves.

Figure 1: When is the optimal retirement date? 65 historical lifecycles, ±2 year window

Three key findings stand out from this historical comparison:

- The default retirement date is almost never the 'right' one. Retiring exactly at the 30-year mark was optimal only 15% of the time. Even a single-year shift often improved the outcome.

- When timing changes, delaying is optimal in most cases. In nearly two-thirds of historical lifecycles, the optimal choice was to retire later.

- The stakes are enormous. The median gap between the best and worst timing choice within the two-year window is two-thirds of the final portfolio value. All four cohorts that ran out of money at the default retirement date could have survived by making a different timing choice within this modest window.

The graphic below shows how widely final portfolio values varied across historical retirement cohorts (i.e., groups with different starting years for their 30-year retirement periods), highlighting how different long-term retirement outcomes were depending on when the withdrawals began. Each bar represents a retiree who started retirement in a different year with the same portfolio value and who followed the same strategy. In this example, all retirees started with $1M portfolios, 60/40 allocations, and 4% constant withdrawals.

Figure 2: Final portfolio value by retirement start year — $1M / 60-40 / 4% constant real withdrawal / 30 years [Created with Bellavia]

Why Does The Retirement Date Matter So Much?

These results can be better understood by looking more closely at sequence-of-returns risk. In practice, that term conflates two related but distinct sources that arise together but can be analyzed separately. Javier Estrada, Professor of Finance at IESE Business School, asked whether sequence risk is really as consequential as commonly believed. The variance decomposition suggests the answer depends on which component of risk is being considered. The analysis separates sequence risk into two components:

- Cohort risk: This is the risk of experiencing a particular set of returns. Someone who retires in the early 1980s receives a very different collection of annual returns than someone who retires in the late 1960s. Critically, even if each person's returns were shuffled into the best possible order, one set would still produce a better outcome because the underlying return environment in the two periods is different.

- Pure sequence risk: This is the risk that the ordering of a given set of returns works against the retiree. Given the exact same 30 annual returns, the order in which they arrive changes the outcome because of the well-documented relationship between the timing of returns and the timing of withdrawals. In short, early losses are compounded by withdrawals because they reduce the available capital in a way that is not symmetric with early gains.

Once these two components of sequence risk are separated, the next step is to estimate how much each one contributes to retirement outcomes. This is where a standard statistical result called 'the law of total variance' can be useful.

The analysis examines retirement outcomes in two related ways. The first compares 97 historical retirement cohorts, each starting with the same portfolio, to isolate how much variation in outcomes comes from the market environment itself versus the ordering of returns within that environment. The second links accumulation and withdrawal into 67 complete lifecycles to show how portfolio size at retirement relates to final retirement outcomes.

The first part uses a variance decomposition based on the law of total variance to separate these two sources of sequence risk. This principle states that the total variance of any outcome can be decomposed into two elements: the variance of the conditional means (i.e., between-group variance) and the mean of the conditional variances (i.e., within-group variance). Here, each historical cohort defines a group.

The within-cohort variance is estimated empirically by performing 5,000 random permutations of that cohort's 30 annual returns and calculating the retirement outcome for each permutation. The mean outcome across those permutations captures the cohort effect, while the variance across permutations captures pure sequence risk.

Cohort Risk Dominates Most Retirement Outcomes

Approximately three-quarters of the variation in retirement outcomes arises from cohort risk – that is, the market era the retiree enters. Only about one-quarter comes from the ordering of returns within a cohort.

This helps explain why a two-year flexibility window can be so powerful. It is the only planning lever examined here that can directly change which cohort the retiree enters. By contrast, withdrawal strategies, guardrails, dynamic spending rules, and asset allocation adjustments all operate within a given cohort. In that sense, they address the smaller one-quarter share of the risk, not the larger three-quarters share.

Empirical work on first-decade returns has shown that the first 10 to 15 years of retirement returns largely determine whether a withdrawal strategy succeeds or fails. The variance decomposition provides a formal explanation for this pattern. The returns in those early years are fundamentally a cohort property – and since cohort risk accounts for three-quarters of all outcome variance, once a retiree enters a poor return regime, the remaining years of mean reversion may not be enough to rescue the outcome.

This result holds across every allocation tested – from conservative portfolios to all-equity portfolios, with the cohort-risk share consistently between 70% and 83% – and under every withdrawal strategy examined. Whether the retiree uses constant-dollar withdrawals, guardrails, or constant-percentage spending, cohort risk remains the dominant force in the historical data.

The graphic below shows how a 20% decline affects the final portfolio value depending on when it occurs in the accumulation-withdrawal cycle. The largest effects appear near the end of the accumulation period and near the beginning of the withdrawal period, when portfolio sensitivity is highest. This helps explain why retirement timing matters so much: the transition into withdrawals occurs at one of the most sensitive points in the entire lifecycle.

Figure 3: Sensitivity to a −20% shock by year position — accumulation vs decumulation, averaged across 97 cohorts

Ultimately, you can't escape the period you live in. Which means that once a retiree enters a weak return environment, the other levers available may help manage the outcome, but they cannot fully offset the effect of that starting point.

The Retirees Who Look Most Ready May Be Those Most At Risk

If the retirement date matters this much, the question then is, "Which clients are most vulnerable to poor timing?" The answer seems counterintuitive at first. One of the most important practical findings in this analysis is that the cohorts with the strongest accumulation outcomes – generally those made up of the wealthiest clients who have done best during their savings years and appear most ready to retire – are often the most vulnerable to poor retirement timing. This applies to cohorts collectively, not to comparisons among individual clients.

To see why, we consider complete lifecycles: 30 years of saving $10,000 per year, followed by 30 years of withdrawals at a constant inflation-adjusted rate of 4% of the accumulated portfolio. In our simulation, the four cohorts that ran out of money during retirement had nearly twice the accumulated wealth at retirement ($2.01M mean) as the cohorts that survived ($1.02M mean). More broadly, the correlation between accumulated wealth at retirement and final portfolio value after 30 years of withdrawals is strongly negative (−0.86). This relationship can be seen by comparing the graphic shown earlier, titled "Final Portfolio Value by Retirement Start Year", with the accumulation graphic below.

The graphic below shows how widely accumulated wealth varied across historical savings cohorts (i.e., groups with different starting years for their 30-year accumulation period), highlighting how different the retirement starting points were across the sample. Each bar represents the accumulation outcome of people who followed the exact same saving plan starting in different years.

Figure 4: Final accumulation value by starting year — $10K/year constant real deposit, 100% S&P 500, 30 years

Comparing the final portfolio graphic shown earlier ("Final Portfolio Value by Retirement Start Year") with the one above ("Final Accumulation Value by Starting Year") helps illustrate an important historical pattern. The conditions that produced especially strong late-stage accumulation results – long bull markets, rising valuations, and growing investor confidence – were often followed by weaker first-decade returns. For example, during the period 1931–1941, the graphic above shows that the accumulated portfolio values were high. At the same time, the earlier graphic showing final portfolio value by retirement start year over the same period shows portfolio values that are relatively low. In other words, some of the cohorts that entered retirement with the largest starting portfolios did not go on to experience the strongest retirement outcomes.

The two graphics discussed above ("Final Portfolio Value by Retirement Start Year" and "Final Accumulation Value by Starting Year") show the accumulation and retirement phases independently. However, linking actual historical accumulation periods to the decumulation periods that immediately followed them helps clarify the pattern between retirement wealth and final outcomes. A saver who began in 1901 accumulated for 30 years and then retired in 1931; a saver who began in 1937 retired in 1967; and so on through 1967–1997. This produces 67 complete lifecycles in which both phases use actual historical market data rather than simulated returns.

This connected-lifecycle methodology also helps explain the strong negative correlation (−0.86): bull markets that inflate portfolios late in the accumulation phase can also raise valuations, which can compress the forward returns available during the first decade of retirement.

We can think of this as a consequence of how mean reversion works in markets. This contrast becomes clearer when looking at two historical savers whose accumulation and retirement outcomes moved in very different directions:

- Mason started saving for retirement in 1953 and accumulated just over $400,000, a below-average result. But he retired in 1983, at the beginning of the greatest bull run in American history, and ended with nearly $2.7 million after 30 years of withdrawals.

- Dixon started saving for retirement in 1937 and accumulated over $2.1 million, nearly five times more than Mason. He retired in 1967 into the stagflation era. Starting with a portfolio five times larger, he ran out of money before the 30-year mark.

The implication is that a whole cohort of retirees who may 'look ready' on paper, with a large portfolio, a long savings history, and apparent financial security, may be the ones for whom the right call is "Not yet" or "Let's plan conservatively."

How To Evaluate The Retirement Environment A Retiree Is Entering

Obviously, no one can predict the future. Still, it's possible to assess whether the current environment resembles the historical periods that led to weaker retirement outcomes. Despite the absence of guaranteed outcomes, there are diagnostic signs that can help.

How Predictive Are First-Decade Returns?

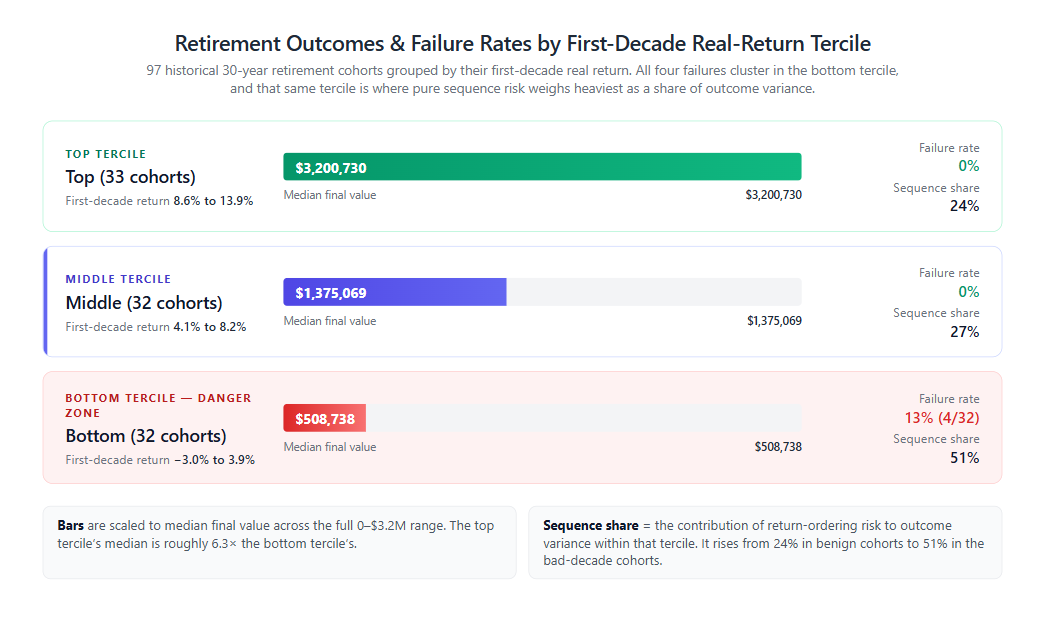

Grouping the 97 historical cohorts by their first-decade average real return reveals a clear separation in both failure rates and final outcomes:

The above table shows all four historical failures occurring in the bottom-third real return group. No cohort with a first-decade average real return above 3.9% has ever failed at a 4% withdrawal rate. Moreover, the top-third median ($3.2M) is more than six times the bottom-third median ($509K). No common strategy adjustment can bridge a gap of that magnitude on its own.

Within the bottom third, pure sequence risk accounts for over half of outcome variance – roughly double its share in favorable environments. This is the kind of scenario where dynamic withdrawal strategies may be especially useful.

Can The Shiller CAPE Ratio Predict Retirement Risk?

The Shiller CAPE (Cyclically Adjusted Price-to-Earnings) ratio is the ratio of the S&P 500's current price to its average inflation-adjusted earnings over the previous ten years. A high CAPE ratio indicates that stocks are expensive relative to their long-term earnings power and has been associated with lower subsequent returns over the following decade.

First-decade returns are known only in hindsight, but there is at least one tool that can help assess the probability that the current environment falls into the bottom third of historical cohorts. The Shiller CAPE ratio shows a strong relationship between starting valuations and subsequent returns ("Resolving the Paradox – Is the Safe Withdrawal Rate Sometimes Too Safe?", 2008). Among cohorts that retired with an elevated CAPE, a disproportionate share fell into the bottom third, and three of the four historical failures occurred in that group.

So, the diagnostic question is not "What will the market do?" but rather "Does the current environment resemble the historical periods where the 4% rule failed?" That is a question that can be approached with some confidence, even if the actual outcome cannot be predicted.

Three Strategies For Acting When Retirement Timing Looks Risky

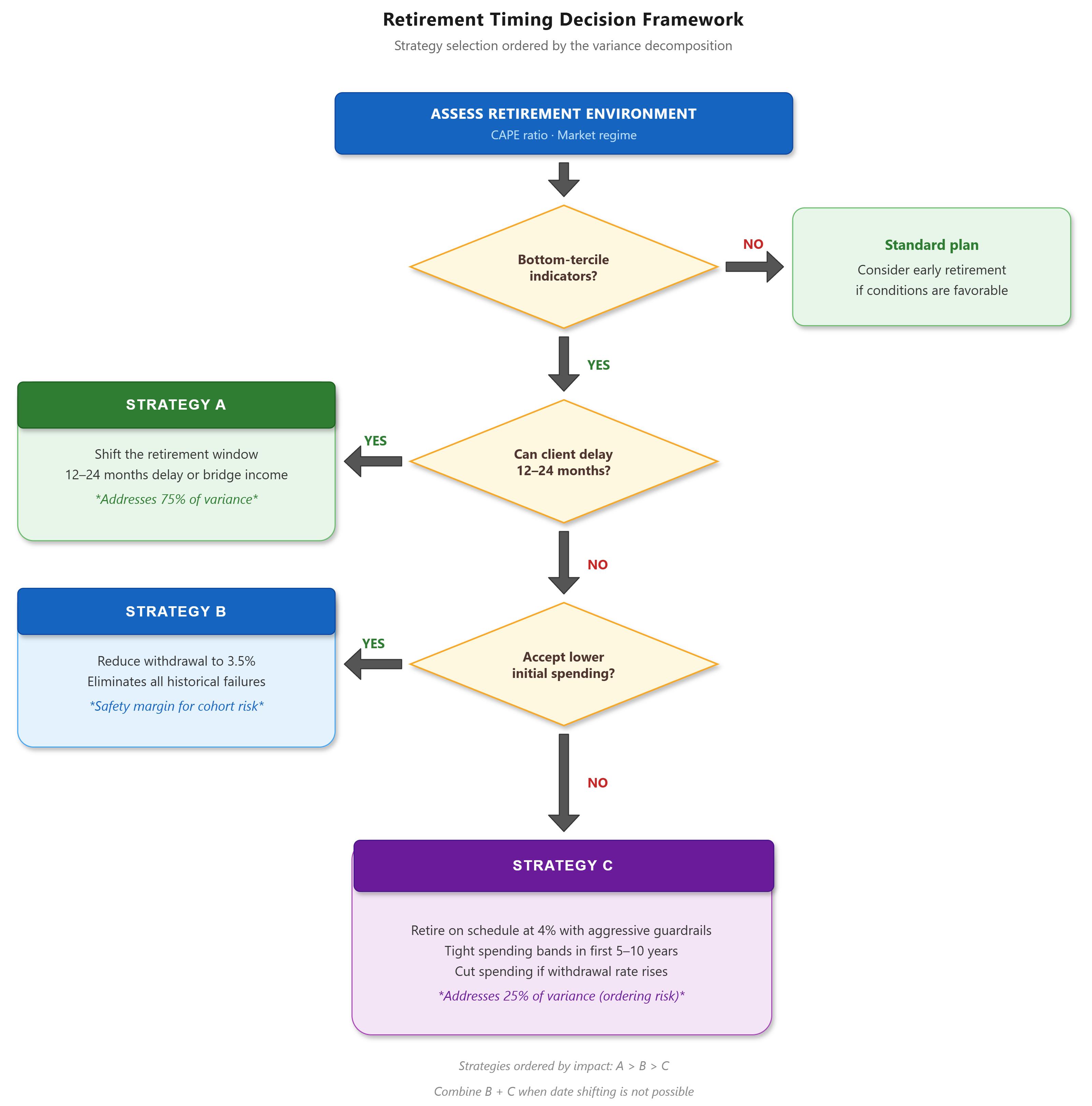

When the diagnostic suggests a retiree may be entering a bottom-third return environment, three levers are available. The priority ordering follows directly from the variance decomposition, which showed that roughly three-quarters of retirement outcome variability is driven by cohort risk, while the remaining quarter is attributable to the ordering of returns within a cohort.

Strategy A: Shift The Retirement Date (Addresses Cohort Risk)

If the target retirement date has some flexibility, even 12 to 24 months, the most effective intervention is to shift the retirement date itself. This is the only strategy that directly changes which cohort the retiree enters.

The retiree can continue working, even part-time, while monitoring how the market environment unfolds. Each additional year of deposits and deferred withdrawals has a compounding benefit: the portfolio continues to grow, and the plan gains a full year of market data for reassessment.

For retirees who cannot continue full-time work, there are bridge strategies: part-time consulting, phased retirement, or drawing on a small cash reserve. These can provide the same cohort-shifting effect. The goal is to avoid locking in a 30-year withdrawal plan at what may be an unfavorable entry point for a 4% withdrawal rate, for example.

The window works in both directions. When conditions resemble a top-third return environment – that is, moderate valuations and no signs of a regime shift – there may be a case for retiring earlier than planned, capturing a favorable entry point.

Market timing, in the traditional sense, involves moving in and out of equities based on short-term predictions about market direction. The retirement date decision is different: it is a one-time, high-stakes choice about when to begin a multi-decade withdrawal plan. Retirement planning inevitably incorporates market conditions at every step. Setting a withdrawal rate based on portfolio size implicitly conditions the plan on market history.

CAPE-adjusted safe withdrawal rates use valuations to calibrate spending. The retirement date decision extends this same logic to one more variable. The two-year window is deliberately short, and the analysis shows that modest flexibility tends to have high value. This is different from the always-true statement that it's 'financially better to keep working'. At the same time, delay has real costs: forgone retirement years, continued work stress, and the risk that health issues arise before the retiree can enjoy retirement at all.

Strategy B: Reduce The Initial Withdrawal Rate

For retirees who cannot shift the date, the next most effective lever is the initial withdrawal rate. At a 3.5% withdrawal rate, down from 4%, the historical failure rate among bottom-third cohorts drops from 13% to zero. Not a single bottom-third cohort failed at that rate. Even a withdrawal rate reduction to 3.8% eliminates three of the four historical failures. In other words, when market conditions have been especially favorable, it may make sense to plan conservatively.

The cost is a lower initial income; for example, $35,000 instead of $40,000 per year on a $1M portfolio. At the same time, the retiree can still increase spending later if the first decade unfolds more favorably than the diagnostic suggested.

Strategy C: Apply Aggressive Dynamic Rules (Addresses Ordering Risk)

If the retiree can't shift their retirement window and retires on schedule at 4%, the remaining defense is to focus spending adjustments for the first 5 to 10 years. Within the bottom third, pure sequence risk accounts for over half of the outcome variance. This is the scenario where guardrails and flexible spending rules, including the extensive work by Kitces and Pfau on dynamic strategies, are most directly applicable.

The key insight from the decomposition is that dynamic rules should be understood as insurance, not as the primary strategy. They address the smaller share of outcome variability attributable to ordering. They cannot fully overcome an unfavorable cohort. But within a bad cohort, they can be the difference between survival and failure.

There is an important asymmetry worth highlighting here. At a standard withdrawal rate the average historical retiree finishes with nearly three times the starting principal — what one 2019 study termed "The Extraordinary Upside Potential Of Sequence Of Return Risk In Retirement". Dynamic rules can help capture this upside in favorable cohorts by increasing spending as the portfolio grows. The result is that the retiree can benefit from favorable conditions rather than leaving behind an unnecessarily large estate. But because the downside is dominated by cohort risk – which guardrails cannot fully address – Strategy A's approach to shift retirement dates may still be preferable. The reason is that guardrails avoid ruin by cutting spending – a necessity that could itself be avoided by adjusting the retirement date.

The illustration below summarizes the three-part decision framework, showing how the recommended strategies shift depending on the retiree's flexibility and the share of retirement risk each approach addresses.

What This Looks Like In Practice

One of the more difficult realizations in financial planning is recognizing that someone who appears financially ready to retire may still face conditions that warrant caution. Using a data-backed framework makes this assessment easier to navigate.

For example, consider a retiree with a $2M portfolio asking, "Can I retire now?" Under a conventional approach, the answer is straightforward: $2M at 4% generates $80,000 per year, well above many common spending benchmarks. The next step would be confirming readiness and deciding how best to implement the plan.

However, depending on market conditions, a more nuanced look at retirement timing options may be necessary. The reasoning here may be, "This retiree's portfolio is large because the recent market has been strong. That same market strength is exactly the historical pattern that precedes bottom-third first-decade returns."

Implications For Retirement Planning Practice

By breaking retirement risk into cohort risk and pure sequence risk, our variance decomposition analysis suggests a hierarchy for retirement planning decisions that differs from the conventional workflow.

In this new decision hierarchy, the retirement date becomes the highest-leverage decision. Having even a two-year flexibility window around the retirement date improves median outcomes by roughly 40% in final portfolio value for otherwise identical retirees. It is also the only lever that directly addresses cohort risk.

The initial withdrawal rate, calibrated to the current valuation environment, is the second lever. It can provide a margin of safety against an unfavorable cohort when shifting the date is not possible. Even modest reductions had large effects on failure rates in the historical record.

Dynamic withdrawal rules – guardrails, flexible spending, and related approaches – are the third lever. They address ordering risk, which accounts for roughly one-quarter of overall variance, compared with the roughly three-quarters attributable to cohort risk. Within the bottom third, however, ordering risk rises to about half of the variance, which is where these strategies matter most.

Taken together, the decomposition results suggest that planners may benefit from starting with the retirement date and working backward, treating timing as a key strategic planning variable rather than simply as a fixed constraint.

This reframing asks planners to give greater weight to a variable that has not traditionally been as central in retirement planning. But the historical evidence suggests that it may deserve a larger role. Retirees who appear most ready to retire on paper may still be vulnerable to poor timing, and having 'enough money' may not be sufficient to resolve the question of when to actually retire.

Try It Yourself

Want to test how a one- or two-year shift in your retirement date would have changed historical outcomes for your portfolio? Bellavia's calculator backtests any retirement plan against 150+ years of market data, including the cohort terciles and CAPE-based diagnostics discussed here.

Frequently Asked Questions

Should I delay retirement if the market is overvalued?

Often, yes — at least consider it. Across 97 historical 30-year cohorts, retiring into an elevated-CAPE environment disproportionately produced bottom-third outcomes, and three of the four historical 4%-rule failures occurred after elevated CAPE readings. A 12-to-24-month delay gives the portfolio additional growth and lets the planner see another year of market data before locking in a 30-year withdrawal plan. The cost is real (lost retirement years, work stress, health risk), so the decision isn't automatic — but elevated CAPE is a strong reason to keep the retirement date flexible rather than fixed.

How does the CAPE ratio predict safe withdrawal rates?

The Shiller CAPE (Cyclically Adjusted Price-to-Earnings) ratio compares the S&P 500's current price to its inflation-adjusted earnings over the previous ten years. Historically, an elevated CAPE has been associated with weaker first-decade real returns — and first-decade returns largely determine whether a withdrawal strategy succeeds. Among historical cohorts that retired during elevated-CAPE periods, a disproportionate share fell into the bottom-third return tercile, which is where 4%-rule failures concentrate. CAPE doesn't predict any single year's returns, but it shifts the probability distribution of the cohort the retiree is entering.

What's the difference between cohort risk and sequence-of-returns risk?

Sequence-of-returns risk in retirement actually combines two distinct risks. Cohort risk is the risk of experiencing a particular set of returns — for example, retiring into 1970s stagflation versus the 1980s bull run. Even with the best possible ordering, a bad cohort produces a worse outcome than a good one. Pure sequence (or ordering) risk is the risk that within a given set of returns, the order works against the retiree, because early losses combined with withdrawals reduce the capital base asymmetrically. Variance decomposition across 97 historical cohorts shows cohort risk drives roughly 75% of outcome variance — about three times more than pure ordering risk.

Does retiring just before a market crash mean retirement failure?

Not automatically, but it dramatically raises the risk. Historically, retirees entering a bottom-third return environment had a 13% failure rate at a 4% withdrawal rate — versus zero failures for any cohort whose first-decade real return exceeded 3.9%. Three mitigations help: (1) shifting the retirement date by 12-24 months can move the retiree into a different cohort entirely; (2) reducing the initial withdrawal rate from 4% to 3.5% eliminated all historical bottom-third failures; (3) dynamic withdrawal rules (guardrails) can preserve outcomes even within an unfavorable cohort, though they can't fully offset cohort risk.

References & Sources

Safe Withdrawal Rate Foundations

-

Bengen, W.P. (1994). Determining Withdrawal Rates Using Historical Data. Journal of Financial Planning, October 1994.

-

Pfau, W.D. (2011). Safe Savings Rates: A New Approach to Retirement Planning Over the Life Cycle. Journal of Financial Planning, May 2011.

-

Blanchett, D., Finke, M., & Pfau, W. Optimal Withdrawal Strategy for Retirement Income Portfolios. Morningstar Investment Management Research.

Sequence Of Returns Risk

-

Estrada, J. (2021). Whether Sequence Risk Is Really As Important As Commonly Believed. Journal of Investing, Vol. 30 No. 6, p. 47.

-

Kitces, M. (2014). Understanding Sequence Of Return Risk – Safe Withdrawal Rates, Bear Market Crashes, and Bad Decades. Kitces.com — Nerd's Eye View.

-

Kitces, M. The Extraordinary Upside Potential Of Sequence Of Return Risk In Retirement. Kitces.com — Nerd's Eye View.

Dynamic Withdrawal Strategies

-

Guyton, J.T., & Klinger, W.J. (2006). Decision Rules and Maximum Initial Withdrawal Rates. Journal of Financial Planning, March 2006.

-

Pfau, W.D., & Kitces, M.E. (2014). Reducing Retirement Risk with a Rising Equity Glide Path. Journal of Financial Planning, 27(1), 38–45.

CAPE Valuation And Withdrawal Rates

- Kitces, M.E. (2008). "Resolving the Paradox – Is the Safe Withdrawal Rate Sometimes Too Safe?" The Kitces Report, May 2008.

Historical Market Data

- Robert Shiller's U.S. Stock Markets 1871-Present and CAPE Ratio, Yale University.

Originally Published

- A version of this article was originally published as a guest contribution on Kitces.com — Nerd's Eye View.

Discussion (0)

Join the conversation

Log in to commentNo comments yet. Be the first to share your thoughts!